I wrote this post earlier on in November, in preparation of my speech at second Shenzhen (China) International Industrial Design Fair, where I was asked to talk about the role of Openness and Platforms in the Manufacturing industry, in the so called age of Makers. China looks an increasingly exciting place-to-be for those interested in re-thinking manufacturing. 30 years of optimizations left there a strong, reconfigurable, efficient and collaborative manufacturing ecosystem that looks an ideal place to experiment in open manufacturing as many are already doing. It will also depends on politics obviously, but I think China has a chance for a leadership in this shift. The post follows after the slideshare embed. Will help you understand much more of the presentation. This post, partially amended, first appeared in Italian on CheFuturo.

—-

Just few weeks ago, a wonderful, about half an hour, documentary – amazingly directed by my friend Tristan Copley Smith – was eventually published. This great piece of work, was shot in Barcelona – the Fab City – earlier in 2014, around the beginning of July, during Fab10: the 10th edition of international Fablab conference.

It was during Fab10 – and the fateful moment is well documented in the video – Mayor Xavier Trias pressed a button and virtual triggered a 40 years countdown: as explained in the video by Vicente Guallart – urbanist and chief architect of the Barcelona municipality – this countdown separates the city from the moment in which it will be globally connected yes, but locally self-sufficient. This narrative is described as the switch from PITO (Product In Trash Out) model to DIDO (Data In Data Out) model.

Another key resource which saw le light recently, was the fifth edition of the Journal of Peer Production , an independent publication that looks into the potential of, peer to peer models. This issue was dedicated to the so-called “shared machine shops” – places where – as in Fablabs – you share machines and skills to help you fabricate, modify and hack tangible objects and doing this also looked into potential, cultures and limitations of the “makers” movement worldwide.

Rethinking an old production model

Despite 40 years can be many, radically rethink a production model is an enormously complex challenge. Apparently, challenges go far beyond reach of the most optimistic predictions of the potential of Fablabs and makers alone: this for a set of reasons ranging from – still existing – technology gaps to poor “political” awareness of the movement itself.

In a crucial passage of the opening oped of the Journal, Peter Troxler brutally analyzes the level of understanding that Makers and DIYers have of the complexity of industrial production:

We are so ignorant of the complexity of goods around us that anything beyond assembling a puzzle or an IKEA furniture can be hastily baptized as a DIY achievement […] More pleasant than the mere use of a consumer good, autonomy becomes synonymous with assembly and repair [but] the kit empties DIY of its substance, like a marketing bundle.

In further considerations Troxler explains how makers and fabbers could become nothing but than superconsumers, requiring even more complex products (enabling and extremely customizable) to producers who are thus confronted with technological and design challenges even more:

[…]the tools used and claimed by the “creative and innovative” often mean exactly the opposite for their producers. Without going as far as extracting the necessary minerals for the manufacture of electronic components, it’s hard to imagine that this process is self-managed and fun.

What simplicity is for users, is simplexity for engineers: “making things easier to the user necessarily means having to make them more difficult to the engineer who invents them.”

The issue

Understand how peer to peer, open, collaborative models can play a credible role in the manufacturing industry is key to the extent that such models proved deeply transformative in digital industries. But, where should we start from?

The dominating competition dynamic brought us to the current product manufacturing landscape low margins, slow innovation: think about your washing or your refrigerator, how much did they really evolve in more than a century? Wholly produced – or at least partially – in common factories, with common skills and common machinery by so-called OEMs (Original Equipment Manufacturer) competing with each other, these products are almost all different, but all the same.

Indeed, to produce more revenues and provide a low-risk investment perspective, mass production runs on two approaches: the first is obviously that of increasing numbers. The costs of building a product line – tooling- impacts less is size of production increase as so does the profitability of each single piece: producing 100 products of a kind is much less efficient than producing 1000000. Globalization has been the key strategy to achieve such scalability: creating consumers alike around the world allowed to extend revenues, substantially without risks (and real investments in transformative innovation).

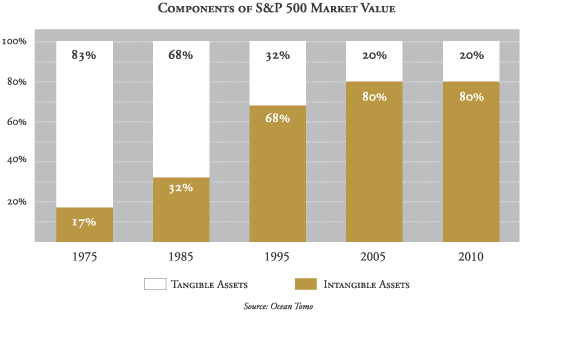

On the other side, companies differentiate themselves from the competition increasingly thanks to brands and narratives, reinforced not only by the quality of the products but also by considerable investment in marketing, advertising and storytelling: in the last 35 years, much of the value of the S&P 500 just moved from tangible assets (such as factories ) to brands and intangible assets (stories, consumer trust, brand image).

If, therefore, on the one hand we have been accustomed to thinking that industrial production is market sustainable only if the numbers are big, we see that on the other hand companies themselves tend to become intangible and therefore consider tangible aspects (the “factory”) as a low value phase, which they attempt to entrust to partners and suppliers: can we really say that Apple physically makes iPhone?

But the landscape has changed

State that we Europeans have a very peculiar point of view on such issues – we live in technologically advanced countries going through a huge systemic crisis; but certainly, from our point of view, we can say that the cultural framework and expectations are radically changing. At least four trends increasingly push towards products digitization and the triumph of intangible value over tangible one:

- Hyper Reality: we see more and more products like hybrid experiences, online and offline.

- Era of Access: due to changing perspectives on ownership and cash crisis many product evolve into services and then platforms. Car sharing and carpooling are now ubiquitous in European cities and Uber just reached 40 Billion valuation.

- New Environmental Ethics: users are more aware of the impacts that consumption habits have and try to be more environmentally savvy: a collective karma of urgency to change is spreading

- Ultra-personalization: mass market customization – coined by Paul Eremenko head of Project Ara Google – is the idea that products are in fact eco-systemic customizations (that may be tribal, local and DIY) based on a shared platform. According to Eremenko up to one quarter of product value is in “user-customizable features”.

What should we expect?

From a purely technological point of view there is no doubt that great brands are largely moving into on demand, distributed and digital manufacturing and 3D printing. HP recently announced its new Multi Jet Fusion Technology holds great if not revolutionary promises. Autodesk, among the most innovative companies in the world, just launched a fund $ 100 Million for 3Dprinting startups.

On a political layer environmental protection regulation may be soon adopted globally: recent agreements between the US and China on climate positively anticipated the meetings that will take place in Paris in July of 2015 and have set goals rather ambitious for the reduction of greenhouse gases: it is still unclear whether the achievement of these goals will go through the application of a Carbon Tax but it is plausible that restrictive policies on use of fossil fuels could be soon adopted. According to The Guardian, Bank of England will soon “conduct an enquiry into the risk of fossil fuel companies causing a major economic crash if future climate change rules render their coal, oil and gas assets worthless”. The case such a environmental friendly regulation takes place is a perspective that becomes more and more credible today. Such regulations would impact primarily on logistic models and, inevitably, would push toward a more responsible manufacturing, which would be more frugal and certainly more decentralized.

In addition an increasing the number of public actors (eg: industrial districts or local policy makers) are interested in developing policies designed to bring manufacturing jobs back to retrace the same globalization processes backwards after having encouraged it over the years.

Meanwhile the bottom-up community of Fablab and makerspace is growing exponentially, already more than 430 – only 350 in July during Fab10 – and may certainly play a role to the extent that it will provide an idle production capacity especially for objects which are designed in a partially different and more “hackable” and repairable way. As rightly said a from my friend and father of Slic3r, Alessandro Ranellucci (edited for clarity):

“given the opportunity to create or retain economic value locally, it looks all very difficult (and perhaps a bit ‘daunting) if we reason in terms of replacement of existing products as we know them – a field on which we have still much to do. Perhaps we need to think in terms of meeting the same needs with new products”

Besides all this we are already seeing new models for the aggregation of locally available production capacity. Although it is closely related to OpenDesk, the English project Fabhub is already a network of production (which aggregates dozens of makers spread almost all over the world) and that could be potentially available for other brands once “unbundled”.

Even in the US, however, projects like Maker’s Row or Britehub are doing more or less the same thing and taking shape as an effective tool for local production, for now intended to creatives and small size brands.

Do not underestimate the role that also true on-demand manufacturing services may have in the future, thanks to improved manufacturing technologies and digital additive manufacturing. Shapeways, a company of Dutch origin that already offers many opportunities for small sizes products on demand manufacturing (from art, to home tools), already slipped on two continents and has its Factory of the Future scattered between Europe and the two coasts of the United States, in an apparent effort to reduce logistics impacts.

They could then one day these players become a new option, a new type of contractor, for global brands and not just small actors ? The question might be asked is: what direction will, in a few decades, these same global brands?

Why do we need to move from Open Innovation in a closed company to shared innovation in open companies?

Besides, the more the (manufacturing) market is digitalized, the more it follows mechanics that I recently explained in a recent piece and will briefly recall. Digitally enabled markets follow the power law (also known as the “Long Tail”) and three roles are available (I will try to tie them to examples in this industry, in order to make it clearer):

- The micro markets of the LongTail: products and services marketplaces where you compete on speed and elasticity and create and nurture niches; brands are short lived and ephemeral and players are small (for example, a designer who creates a product for his fan base).

- The enabling infrastructures: aggregation platforms that offer routine processes (eg. logistics) and support small fragmented players (eg: on demand manufacturing services).

- The customer relationship business: agents that connect and understand market expectations and help products to be created (es: kickstarter or the Arduino community)

In the classic definitions of Open Innovation (those of Henry Chesbrough in “Open Innovation: The new imperative for creating and profiting from technology“) it’s said that ” firms can and should use creative ideas and paths to the market, which are both internal and external, when trying to innovate their technology ” and ” innovate by sharing risk and rewards with partners ” and the boundaries of the firm with society and the ecosystem become more permeable. In the n evolution of the concept of open innovation into what I call shared innovation production companies and brands will have to look at two main challenges.

On the one hand, player from supply chain and infrastructure will need to increasingly be designed as multi stakeholder and cooperate with communities and local governments increasingly configuring as opportunities in their eyes (local jobs). Firms operating in this context will need to leave sub-processes of the manufacturing cycle, such as distribution, post-sale servicing and customization to local players embracing more participative and equitable profit generation chains which are inherently more sustainable ecologically and socially wise. If you choose to operate in infrastructures, it will be important to aggregate production capacity and do so in a transparent and open way at some point exposing APIs that allow to integrate “unbundled” production schemes into far more complex business processes.

On the other hand “interface” products and services will need to be creativity enablers and for meaningful innovations residing in niches and digital communities: consumers become makers and eventually citizens of a new world we’re all called to participate building. In this cultural space open (source) is a key factor in enabling creators to use and rethink technologies.

Finally, if you work in the area of customer relationship, it will be important to know how to link creativity to opportunities as platforms such as Kickstarter or Quirky are doing, helping a growing base of intelligent communities and creators build a new generation of products.

As Alain De Botton said recently, to build a better version of capitalism – that is able to look at the true needs and do so in a responsible manner – is a huge growth opportunity. Starting with manufacturing is possible and indeed someone is already working on it.

(Disclaimer: I’m involved in OSVehicle)

If you liked the post, please: Tweet!

Follow @meedabyte

Nice post, I’ll share it.

Pingback: From _PRODUCTS In & WASTE Out > to _DATA In & DATA Out >

Pingback: Open Source Circular Economy Days | From PRODUCTS In & WASTE Out to DATA In & DATA Out