Quite recently I’ve had the chance to participate to Pisa’s Internet Festival, one of the biggest Italian event about the Internet (as per the name). I was the curator of an entire conference afternoon that was dedicated to the theme of the sharing economy (or the collaborative economy as I very much more like to call it lately).

As you may have noticed, this topic (which I introduced thanks to the presentation you can find here) is a fairly present trend, in a way, it’s a burning one.

Everybody has a rant about the Sharing Economy so here’s mine.

For some time now a lot of articles have debated about what the so called sharing economy is at heart: is that a “movement” of peers who learnt how to cooperate thought more and more disintermediated infrastructure? Or is it just a plainly new market for venture capitalists?

Recently, while commenting AirBnb’s Douglas Atkin presentation of Peers – a much discussed, self dubbed, grassroot initiative that promotes amendments to public policies to eliminate frictions between the sharing economy and exiting entrenched interests (or laws) – Tom Slee, a regular Sharing Economy commenter – puts it like that, with no frills:

Going through Crunchbase tells me that the total funding for the 40 partners [of peers] is over $600M. AirBnB has received $120M, including funding from Andreessen Horowitz, Jeff Bezos, Ashton Kucher […] almost all the funding is going to the Bay Area or New York. The non-profits in this organization are being taken for a ride by the appealing anti-establishment language of Silicon Valley.

And more directly:

Venture Capital funds are not interested in people power, they are interested in an investment with a good return. The fact that Douglas Atkin doesn’t once mention the financial motivations of the forces behind the sharing economy is either dishonest or unbelievably self-deceiving.

Now, to be honest, collaborative or cooperative approaches to generating wealth, value and tangibles production is not new at all. The amazing talk by Marjorie Kelly (with transcript) you can find here, has an impressive coverage of what she calls generative ownership, and it may be a useful read for those that are not aware of what that these models are already able to achieve.

Furthermore, if we think to the “digital” ancestors of the model, they were actually born in the late seventies, largely before the explosion of the internet pervasiveness that now, decades later, is eventually giving disruptive traits to the phenomenon.

All, in fact, was born from Stallman’s Free Software movement: for the first time a cooperative, open approach to knowledge creation was confronted with a purely commercial one. Xerox’s interests in keeping a printer program source not accessible faced the interests of the community of developers who had to settle for a poor software. Well, this battle still rages on, after decades, as you may know.

So, the idea of building shared infrastructures of knowledge (such as Wikipedia), or shared enabling platforms (such as Free Software) is not new at all. Even a deep reflection on the commons and their role in society it is really mature if you consider the contribution and work of people such as the Nobel prize Elinor Ostrom, Professor Yochai Benkler, or the incredible contribution coming from P2P foundation founder and long term commons advocate Michel Bauwens, now implementing this vision as research director of FLOK society project in Equador (something you should really look into).

In the past two or three years, however, we have witnessed a growing attention and interest towards everything shared, all that revolves around this magical word, all we typically call now the sharing economy.

As always when there are different views and perspectives, attempts to classification abound: while Michel Bauwens provided an effective and quite radical vision at the OuiShare Fest last May, the sharing economy icon Rachel Botsman recently proposed a classification which, however, is still a bit narrowed mostly focusing on the opportunities for businesses, instead of giving a more holistic view

The truth is that this word (sharing economy) now mostly encompasses, at least in the general even if still niche understanding, a couple of platform models. On one hand we have so called collaborative consumption platforms (where peers exchange access to their idle or underused goods, mostly using renting paradigms), on the other more general P2P marketplaces where you also have selling and, rarely, bartering models applying. The term is also often related to solutions that are supposed to disintermediate transactions thanks to the adoption of the internet as a means of connecting needs and resources in an efficient way.

Behind cultural trends that are here to stay, this huge growth in attention is largely due to the economic (market) success that some of the platforms born in these last few years are currently experiencing. Three sectors lead the pack from a revenue generation perspective: hospitality (a market overly dominated by AirBnB), shared mobility and transportation (with lots of success stories such as that of RelayRides, Uber, Lyft and now also involving corporate players such as Daimler or Avis) and that of fragmented labor (any Task Rabbit out there?).

Despite all this, in parallel with the narration of successes, many now begin to wonder about the impacts (both on a local and global scale) these business models have on society as a whole and what’s their role in the current transition.

The last few months have therefore been characterized by a strong and growing discussion on the topic. As one could expect, the mixed background of sharing, where activism (even political at times) mixes with the world of venture capital and startup culture, easily generates flames. The many articles written recently, also signed by well known and discussed thought leaders as Eugeny Morozov – sorry for the link, requires registration – are here to witness.

I hardly agree with Morozov. But let’s look at the situation honestly. Despite many of these services leverage on globally growing social and human motivations and are presented as ways to supplement incomes in challenging times, they are undeniably created as commercial ventures in a way that is nothing different from all other Venture Capital backed companies, as the often discussed Google, Microsoft or Facebook.

The startup culture indeed, embodies very simple and narrowed principles and it couldn’t be different: exponential growth, maximization of short-term profitability, multiplying capital value by generating “exit” opportunities (the moment in which the original investor sells her equities multiplying the original invested capital). These are the pillars.

The disintermediation (p2p) effect, driven by the adoption of these platforms is normally considered as a very positive characteristic. It gives users the possibility to produce income through the platform itself. One must acknowledge, by the way, that these are not real p2p infrastructures: indeed, despite connecting supply and demand directly, the new mediating actor (owners and designer of these e-marketplaces) just substitutes older monolithic incumbents (such as industry lobbies or governments).That’s not genuinely open and peer to peer and we must at least acknowledge it and understand. This is what Michel Bauwens calls, Netarchical Capitalism:

Netarchical capitalism is a hypothesis about the emergence of a new segment of the capitalist class , which is no longer dependent on the ownership of intellectual property rights (hypothesis of cognitive capitalism), nor on the control of the media vectors (hypothesis of MacKenzie Wark in his book The Hacker’s Manifesto), but rather on the development and control of participatory platforms.

These platforms (I’m investigating a lot lately) are indeed based on forms of reputation and trust (often dubbed as the “currency of sharing”) as opposed to more traditional contexts where consumer (not peer) are trust in compliance law enforcement, and third-party certifications. Think of the world of traditional B&Bs – often available online thanks to the good old classified ads – compared to the user experience revolution brought by players such as AirBnB, or the clones that followed.

The problem now it’s that this middle ground is still almost totally unregulated in many countries. While in some countries or cities we see crackdowns in other cases, more fruitful conversations arecoming up. In spite of this unclear situation some of these player are, as said, gaining financially remarkable results.

In fact an enormous economic opportunity has risen with many complex social implications to be considered. Let’s take the phenomenon known as gentrification, something that is growing all over the place. Let’s say you live in a neighborhood where the touristic attractiveness of your home can generate a lot of money. That makes housing prices rise and people with lower income are pushed out from the neighborhood, and need to move to cheaper suburbs. This is already happening in cities such as NY, San Francisco, London and many others. In other cases a mobile app and a car can transform you into an unlicensed taxi driver. Ok, we all hate the infamous taxi tariffs that exist in most of the cities, but that’s not the only part of the picture we should look into: we need a more consistent and mature phase of legislation.

In fact, it is not uncommon to see power users of these platforms creating illegal (or semi-legal) businesses, substantially thriving out of lack of controls and un-existing or inadequate laws. In fact often generating regimes of unfair competition.

A recent post on Fast Company clearly describes how this is becoming a quite interesting business opportunity for many:

My Airbnb host is leasing three apartments just like this one, all in the same building. He posts two of them on Airbnb, as he does with two other apartments in two other buildings. The third he just acquired, so he’s busy setting it up. When he’s done, he will have a total of six apartments listed […] For this part-time job Bradley could make a six-figure income next year.

Obviously not all the users of these platforms are power users but, increasingly, the platforms owners are pushing to increase professionalism. In a recent post on The Next Web, you can see how Airbnb is pushing for a rising quality standard across the user base:

Not every host is the same and there are those that are exceptionally better than the others. But Airbnb doesn’t appear to want this type of disparity — it wants to ensure that everyone has the same level of care as the other property down the street. Just like how hotel staff maintain a sense of dignity and professionalism when responding to every customer’s request, Airbnb wants to do the same.

It’s time to ask ourselves what’s the right interpretation: is the sharing economy the first attempt to instill community perspectives in the traditional process of venture capital backed innovation? Or, on the contrary, is that an attempt of Venture Capital to monetize peer to peer and cooperative trends emerging from a pervasive internet and a global cultural shift?

Each and every point of view is probably to be respected. However, approaches that really don’t even question the role of private capital in generating shared innovation – before and beyond the trend of the so-called “Sharing Economy” – only can offer simplistic interpretations.

Against the backdrop of uncertainty and lack of dynamism in the economy, VC ecosystems and Startup thinking gained more and more attention lately. A lot comes from the success narrative that surrounds it like a halo, even if criticism is appearing more and more often lately, as Alice Marwick put it few days ago on Wired US:

Digital elitism does not reconfigure power; it entrenches it. It provides justification for enormous gaps between rich and poor, for huge differences between average people and highly sought-after engineers. It idealizes a “better class of rich people” (as Kara Swisher put it) who evangelize philanthropy and social entrepreneurship — but it also promotes the idea that entrepreneurship is a catch-all solution, and that a startup culture is the best way to solve any problem.

Startups competition are popping up every here and there and everyone knows what an equity or seed investment is: everyone wants to be an entrepreneur these days. However, looking at the bigger picture you may realize that the perspective is not always so rosy.

Startups themselves are often considered commodities: they are bought and sold without any real innovation concerned goal. Sometimes startups are even closed down immediately after acquisition simply to prevent a new competitor to arrive on the market.

The dominant approach in the world of private investors is still strongly traditional in fact: it’s genuinely interested in the multiplication capital gains in a rather short term. All this often goes through shares changing hands and ends up, at best, in IPOs that often leave open question marks in the public audience. Share price is frequently considered unnaturally inflated. IPOs themselves are in fact, as Lee Bryant effectively pointed out in this wonderful post, no more than a way to make these companies tradable financial assets.

Therefore we face today a context in which innovation value is often harmed by the (legitimate – as this is the principle our western society is currently based) tendency of capitals to focus on short term capital gains and don’t even care about externalities.

What kind of innovation?

In a recent, extremely effective interpretation of the situation given by Clayton Christensen (and still mediated by the excellent Bryant on PostShift), the thing is very easily explained.

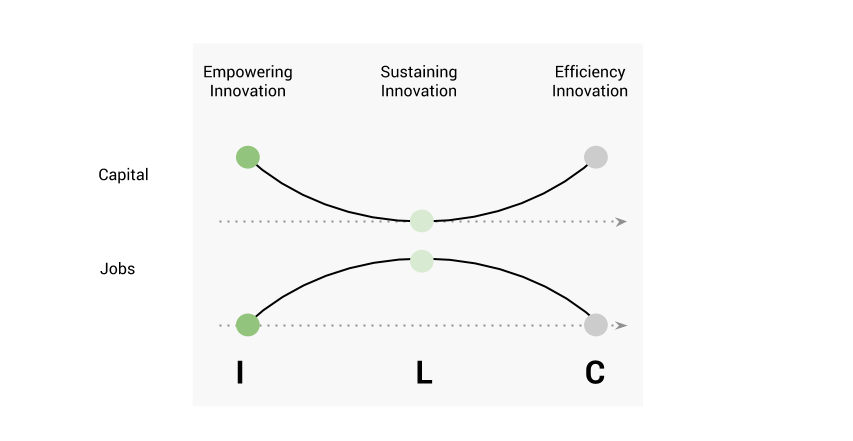

There are basically three types of innovations:

- Empowering Innovations: the cyclical ones that make a technology (or a capability – by means of a technology) accessible, economically wise, to a larger magnitude and order of users. An example is the internal combustion engine vs. the steam engine.

- Sustaining Innovations: innovation that makes the products and technologies better (an example? The ipod vs your old mp3 player).

- Efficiency Innovations: aiming to reduce the price of a technology or capability mainly though production efficiencies (such as in the automation of some of the tasks in a manufacturing process).

It goes without saying that empowering innovation is more complex, riskier and requires capitals to be locked in the investment for longer periods. Marianna Mazzucato effectively dubs the kind of capital needed for empowering innovations as patient capitals.

On the contrary the latter (efficiency innovation) tends to free up capital thanks to the efficiencies it introduces in production (production becomes less capital intensive). In a healthy system, liberated capital should go back, feeding the innovation process.

This way of looking at innovation is extremely straightforward and it shows also a clear convergence with the ILC Innovate – Leverage – Commoditize cycle as explained effectively by Simon Wardley, making it even more clear and credible.

During the first phase (which Simon defines that of uncharted innovation) value is created from chaos and creativity. In the second transitional phase, one takes advantage of maturing technology to monetize a growing market. In the long run a third phase, that of hyper-industrialization, takes over and “lower cost of doing business” triumphs (you compete on price and experience utility consumption patterns). You can easily get the parallel with Christensen thinking:

- Empowering innovation / Innovate phase = Pioneers thrive

- Sustaining innovation / Leverage phase = Settlers thrive

- Efficiency innovation / Commoditize phase = Town Planners thrive

But what’s the problem these days? In this historic moment, private capital seems heavily focused on efficiency innovations. In a way, I think we can also frame the so-called “sharing economy” in this framework. Indeed especially collaborative consumption, that is clearly focused on diminishing idle times and pushing for deregulation (that can be interpreted as a way of making markets more liquid and efficient), can be easily seen that way.

Now, let’s look at one important aspect. I’ve put together a chart to better explain what’s the issue.

You can clearly see how the amount of labor needed relates with the amount of capital required to the three phases. You can also grasp how the prominence of efficiency innovations is harming the labor market as a consequence. Indeed many of us are getting used to the concept of jobless recovery and it’s now maybe easy to understand how while GDP is slowly coming back, the jobs market is not.

Though this perspective it’s not that encouraging – everyone facing a choice would go for impact innovations, decisive in making radical breakthroughs – it must be said that our society still has a desperate need for efficiencies, both from a technological and social processes related standpoint.

It is not long ago that a wonderful piece by David Graeber eminently explained how our organizations are full of “bullshit jobs” that nobody would miss if lost. All these jobs will, inevitably, will disappear in the medium-long term exactly in line with the trends we are talking about efficiency innovation).

So, even if an increased tendency for efficiency innovation could be a good news from certain standpoints (e.g.: resource consumption) the question is rather: why the freed-up capital is not reinvested in search of new Empowering Innovations? Lee Bryant explains:

Whereas finance was once a service to business by providing liquidity, it has come to own business to the extent that investing in innovation is just one possible use for capital among other, less risky and less prodcutive options. Instead of re-investing cost savings derived from efficiencies […], much of that cash is being hoarded or invested in financial instruments, rather than value creation.

Sure enough it’s because, on one hand, we live in a conflicting society. We’re always on the edge of harsh social confrontations. Many are, globally, the frictions related to a potentially upcoming scarcity issues, regarding very basic resources such as food, energy and shelter, water, environmental quality and more. These premises increase risk and eventually argue in favor of protective capital accumulations and conservatives behaviors.

On the other hand, relevant both financial and digital tools provide today a rather favorable outlook for speculative capital: artificial intelligence and big data software is now able to trade financial assets in real time and almost independently, ensuring good returns in very short (seconds) term as this excellent essay from Deloitte explains.

Private capital is currently failing (given the landscape) in the mission of ensuring cyclic innovation and society seems stuck in an endless whirl.

With this clearer picture in mind, the so called “sharing economy” can perhaps be framed better as can the dark sides of it’s mostly VC-Centric incarnations: a rather obvious friction with the existing legislation (often a common trait of innovations) and even negative potential and social impacts, ironically enough as it’s often chanted as a social movement.

Despite all, the signs of social shift towards a less secure and more complex society should be seen as expressions of major, more far-reaching trends we are undergoing as a society and not just as effects (or rather causes) of the explosion of the so called sharing economy.

At this point, the question arises: are we talking about real innovations or unconscious (or maybe conscious) exploitation of communities and people that are losing their basic social rights in the meanwhile? Of course, the picture may not be white or black.

In fact, no doubt people can get significant economic, experiential and social benefits by means of using these collaborating platforms and creating communities: otherwise their success would not be easily explained.

I think it’s time for us to look and act holistically, and responsibly, about these emerging and disruptive business models and service patterns and make them 100% compatible with an existing and evolving social contract.

Way too often our institutions were more concerned with the lobbyists agenda, as the stories of SOPA, PIPA and ACTA tell us, than with citizens expectations. At the end, these threats were escaped thanks to the mobilization of citizens, influencers and, as we need to consider, of big corporations that joined the party.

The most vocal and potent political activity of cyberlibertarians has been the defeat of certain governmental regulations (such as SOPA and PIPA, opposition to which was supported and even coordinated by Google), which have turned out to be less anti-corporate than in service to some corporate agendas while attacking others (especially those of “content providers”).

Likewise today, when these platforms make new use cases possible, it’s our duty as a community (and society) to question and understand the impacts. We must be aware about how every technological transformation impacts on our lives. We may need to interact with legislators directly and even become legislators, avoiding middlemen, as it’s the case with peers.org.

So, perhaps there’s nothing much new behind collaborative consumption and the so-called sharing economy but yet another narrative and marketing strategy by those that legitimately invested money into promising ventures. Unfortunately, these gamechanging and disruptive companies still have a North Star: the “world’s dumbest idea” , as Steve Denning puts it, to generate shareholder value maximization in the shortest time possible, with a social impacts that is accidental to the rules of business.

Just figure it out.

Opening and Disrupting Venture Capital

We live in a world that needs innovations but we are failing to find the proper tools to do so.

The whole point is about being able to innovate in the interest of communities and not only able to free up some capital thanks to efficiency gains.

The point is about supporting longer-term visions and shared resilient perspectives.

The, essentially public, patient capitals that Mazzucato advocates for will continue to play a vital role, especially with an increasing participation of the public to policymaking and national strategies – likely through the birth of new political parties and actors.

In parallel with a rising debate on public spending and national strategies to pursue innovation, we should expect a transformation in private capital and in the role that communities have on it. Indeed what we should hope and, I believe, expect, is a transformation in private Venture Capital dynamics towards more collaborative and inclusive processes.

The first signs of transformation in private capital processes, indeed, already undergoing. I’ll not dig into details about the almost incredible results that crowdfunding platforms are achieving around the world these days but the explosion of approaches to the topic and the number and variety of crowdfunding solutions today is exponential.

In parallel, we have an ever increasing penetration of national legislations dealing with both reward and equity crowdfunding which is the process by which funds are raised in a distributed and cooperative way to build up funding capital for companies.

Other noteworthy trends that in the same way embody more fluid and participatory venture capital processes are coming from the United States: I’m talking about the so-called angel syndication. Syndication is a new possibility created by the framework of the JOBS Act.

Angel list, the main platform that connects early stage investors (angels) and startups, recently enabled these syndicatesfeatures. By means of these features, particularly prominent angels may, thanks to their investing credibility and track record, coordinate other investors and angels and quite easily gain Series A funding capabilities.

However, as perfectly explained by Jason Calacanis in this interesting post, despite this initiative is a step towards more cooperative capital, it’s still a tool in the hands of the very same actors (early stage venture capitalists) than a real disruption.

Much further in the process of building the venture, IPOs are to be considered as well the traditional way of distributing the company capital. IPOs, by the way, don’t really collectivize the strategic management of capital allocation and no mechanisms for an equally cooperatively definition of the venture mission is usually available in that context.

What in fact would be interesting to have, especially in order to assess what kind of investments it may generate, is instead a genuine open source, collaborative and inclusive governance platform for distributed, private venture capital.

It would be liquid feedback applied to investments, on top of cooperative funding models inspired by crowdfunding. This kind of tool – a true Open Source, democratic, P2P, Venture Capital Fund – could probably complement the mission of co-operative banks and credit unions, making capital accessible, scalable and more efficient in supporting community based innovations, being it local, tribal or communal.

As Michel Bauwens puts it in the presentation of the Research Plan of the ambitious FLOK Society project:

As the mutual adaptation between the commons sector, the cooperative sector and the capitalist sector proceeds, the remaining capitalist sector should be increasingly socialized in the new practices, as well as ownership and governance forms.

Indeed, these days digital governance tools and innovative decision making processes are already having a role in helping an amazing variety of things thrive: from political parties to software companies to distributed organizations such as my beloved OuiShare.

We would certainly have many open points to investigate:

- What type of ventures would this open VC fund invest on?

- What idea would such fund have about risk and growth?

- What role would the individual members play and how would the decision-making process go?

Last but not least: would this venture capital be impact and innovation driven rather than profit driven? That shouldn’t be taken for granted.

Inevitably, to make real sense, this type of fund should incorporate a certain level of criticism on the use of capital in support of pure short-term profitability maximization. In fact, alternative capital employment opportunities will always be available that could pay back shorter. Given the competitive nature of investments the decision to invest in community-driven, open funds should have strong motivational roots and feeling of belonging. We would therefore expect this fund to act in line with community’s long-term goals and to be able to repay that community in terms of non purely monetary assets.

The possibility exists that, to further untie this type of investment from the issue of competitiveness with other financial assets (eg: investment funds, bonds, etc. …) you might get to use alternative currencies to the fiat.

The Bitcoin ecosystem is making great strides in this direction and platforms for equity crowdfunding in Bitcoin already exist. The list of Bitcoin ‘stock exchanges’ and Bitcoin equity crowdfunding platforms is growing (see things like TheRockTrading Stock Exchange). However currencies that – unlike Bitcoin – embed demurrage would probably work better: this would make hoarding more difficult and, on the contrary, favor their use in support of shared investments.

As said, it would be very interesting to see whether these cooperative capital funds would end up financing the same ventures traditionally attractive today’s VCs and Angels, as the now infamous digital startups whose importance in terms of innovation is, in some way, indubitable (is it?).

To have a grasp of what it means in terms of capital, to build such ventures, it is interesting to read this piece that did the math about “How much does it cost to build the world’s hottest startups”, you’ll see we are not talking of such a huge amount of money.

I think that a collaborative, open and democratic decision-making process would hardly support such value propositions and probably these funds will not help create the next Facebook (for this I am pretty convinced that private speculative capital will continue to have its traditional role), but I may be wrong.

Perhaps a process that collects, manages and allocates capital in a way that is truly democratic, disintermediated and open source would generate radically new innovations whose traits we are still not able to fully understand today.

Certainly a more conscious and cooperative private capital allocation process that aims to supports empowering innovations is not only desirable but sort of an imperative at today. A good deal of (open) disruption in the field is rapidly getting mature and open source, collaborative, private Venture Capital platforms could be the next big thing in innovation.

To stay on top of updates, you should follow me on @meedabyte.

(una traduzione in italiano è disponibile qui: http://wp.me/p44Li2-I)

Pingback: Lecturas interesantes

It is a shame I had to scroll so far to find the main point/ proposal:

“What in fact would be interesting to have, especially in order to assess what kind of investments it may generate, is instead a genuine open source, collaborative and inclusive governance platform for distributed, private venture capital.

“It would be liquid feedback applied to investments, on top of cooperative funding models inspired by crowdfunding. This kind of tool – a true Open Source, democratic, P2P, Venture Capital Fund – could probably complement the mission of co-operative banks and credit unions, making capital accessible, scalable and more efficient in supporting community based innovations, being it local, tribal or communal.”

I couldn’t agree more. Been thinking about/ planning such stuff for quite a while now e.g. http://uniteddiversity.coop/projects/crowdfunding-cooperative/ 🙂

PS “patient capital” just means long-term (and, in the case of debt, generally low interest) captial http://en.wikipedia.org/wiki/Patient_capital

thanks Josef! Would be super nice to know more. I think we should talk about that.

Pingback: Crowd Coffee: December 17 | Crowdfunding News

Pingback: How to Frame the Sharing Economy Narrative (and Move On … | The Research Platform

Like a son, Tony sought out more stable mentors to align himself with.

Somebody I know attended a presentation at the office by Ameriprise Financial, a

financial advising company. Just how much will you charge

for the services?

Pingback: Epica Etica Etnica Pathos (e Social Innovation)

I have a completely different interpretation of “sharing”. Airbnb’s founders (the story goes) were sleeping on friends’ couches when they came up with the idea. Whereas a hotel guest is given a key to a private room, the sharing economy might put that guest in a room to be shared with someone else and simply charge less. Same goes for Uber. So the economics of sharing vs. autonomy is the point. I think the term works for this interpretation.